Business

‘Gas bomb’ dropped on masses as govt approves massive price hike

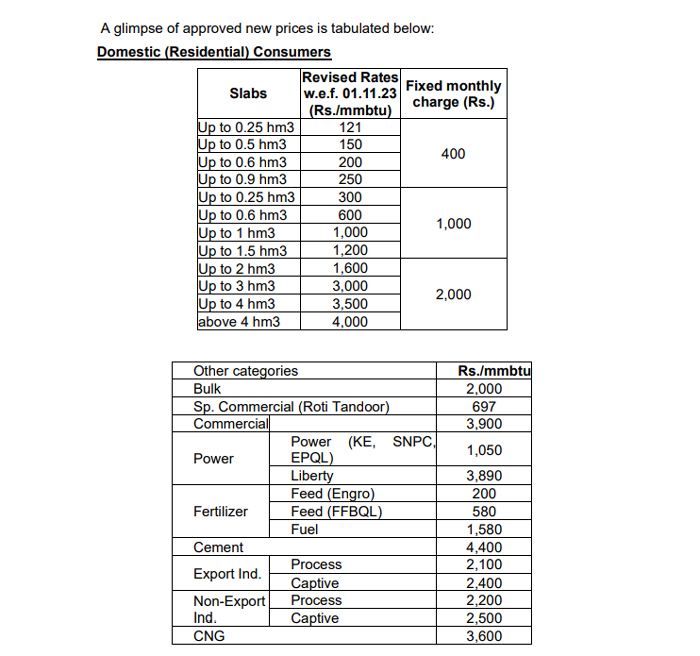

Gas tariff jacked up to 173% for non-protected domestic consumers and 136.4% for commercial users.

- Tariff hiked up to 173% for non-protected domestic consumers.

- Gas rates for commercial users jacked up by 136.4%.

- Monthly fixed charges also increased to Rs400 for protected users.

ISLAMABAD: The caretaker government on Monday dropped a gas bomb on inflation-hit masses by approving a massive increase in gas prices which will come into effect from November 1 (Wednesday).

The government has hiked the local gas tariff up to 173% for non-protected domestic consumers, 136.4% for commercial, 91% for export, and 83% for the non-export industry.

As per the approved summary, the fixed monthly charges for protected consumers were revised upward from Rs10 to Rs400, for non-protected from Rs460 to Rs1000, and for higher slabs up to Rs2000.

The price for non-protected users consuming up to 0.25 cubic meters will be Rs121 per mmbtu, up to 0.5 cubic meters will be Rs150 per mmbtu, for users with 0.60 cubic meters Rs200 per mmbtu, while 0.9 cubic meters Rs250 per mmbtu.

Rates for people using 1 cubic metre of gas per month have been jacked up from the previous Rs400 per mmbtu to Rs1,000 mmbtu.

Those with gas usage of up to 1.5 cubic metres — who were previously paying Rs600 per mmbtu — will now have to pay Rs1,200 per mmbtu.

Meanwhile, small commercial users such as local tandoors will pay Rs697 per mmbtu from November 1.

The power sector will have to pay Rs1,050 to Rs3,890 per mmbtu. The cement industry will pay Rs4,400 per mmbtu.

Rates for the export industry have been set from Rs2,100 to Rs2,400 per mmbtu, whereas non-export industries will pay between Rs2,200 to Rs2,500 mmbtu.

The Power Division, in its press release, maintained that the interim setup had to increase gas prices following Oil and Gas Regulatory Authority’s advice to avoid Rs400 billion being added to the already ballooning circular debt.

The authority highlighted that 57% of the domestic gas connections fall in the protected category where there is no increase in gas price.

“In the name of affordability, some of the most profitable businesses of the country are availing the cheapest natural gas. This has unduly enriched certain sectors while depriving lowest income class including poor farmers and small-scale industries,” the statement mentioned.

Business

The KSE-100 Index has surged by 790 points, resulting in an all-time peak for the stock exchange.

Smog crisis: Punjab will go into complete lockdown, school holidays will be extended

Three Terrorists Are Killed by Security Forces in Harnai District: ISPR

Pakistan’s Climate Change Ministry and GGGI Sign a Pact on Green Finance for Climate Action

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News2 days ago

Latest News2 days agoTo combat terrorism, specific actions are required: Mohsin Naqvi

-

Latest News2 days ago

Latest News2 days agoSmog crisis: Punjab will go into complete lockdown, school holidays will be extended

-

Latest News2 days ago

Latest News2 days agoThree Terrorists Are Killed by Security Forces in Harnai District: ISPR

-

Latest News2 days ago

Latest News2 days agoFertilizer Inventory: Rana Tanveer Expresses Contentment Regarding Stock Availability

-

Latest News2 days ago

Latest News2 days agoOver Pakistan, Rain and Snowfall Are Expected Over the Next Three Days

-

Business2 days ago

Business2 days agoDar chairs the CCOP meeting; Blue World’s bid offer of Rs.10 billion is rejected.

-

Latest News2 days ago

Latest News2 days agoPakistan declares AI chatbots to be dangers to security.

-

Latest News2 days ago

Latest News2 days agoIn October 2024, the SECP registered 2,477 new firms.