Business

Gold retreats from historic high after massive rupee appreciation

- Gold rate (24 carats) falls by Rs2,500 per tola.

- Yellow metal is Rs8,000 per tola “undercost” in Pakistan.

- Commodity breaks three-session winning streak.

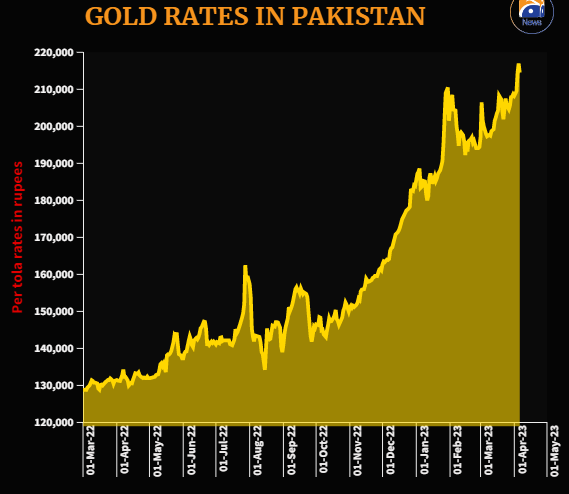

Gold price in Pakistan registered losses on Thursday as the precious commodity retreated from a historic high after investors shifted focus towards riskier assets following positive economic cues in the market, breaking a three-session winning streak.

The depreciation was in line with the rupee movement — which gained ground and closed at 284.42 against the US dollar in the interbank market — and a downtrend in the global markets.

The gold rate (24 carats) fell by Rs2,500 per tola and Rs2,142 per 10 grams to settle at Rs214,500 and Rs183,900, respectively, according to the data released by All-Pakistan Sarafa Gems and Jewellers Association.

The price of the yellow metal was increasing since the last three trading sessions as gold is often hailed as a hedge against inflation.

Pakistan’s monthly inflation in March soared to an all-time high level — 35.4% — from a year earlier, with people feeling more pain from some of the fastest rising consumer prices amid straining budgets as the cost of living continues to outstrip average incomes.

Investors’ attention has now shifted to other markets as the rupee and stocks registered gains following Saudi Arabia’s assurance to the International Monetary Fund (IMF) of depositing $2 billion in Pakistan.

The assurance from Riyadh will play a major role in reviving the stalled bailout programme that Pakistan has been seeking to resume since last year.

Gold price moves in line with the rupee-dollar parity as the country meets almost all its gold demand through imports, and traders follow its international price in setting rates in the country.

Jewellers import the metal against the US dollar and UAE dirham before converting its price into rupees.

The association also mentioned that the price of gold is Rs8,000 per tola “undercost” in Pakistan, compared to the Dubai market, showing that the Pakistani gold market was currently cheaper than the global.

Meanwhile, silver prices in the domestic market remained unchanged at Rs2,450 per tola and Rs2,100.48 per 10 grams.

In the international market, gold price declined by $4 per ounce to settle at $2,019.

As of today, the F-8 Underpass is now open to traffic. Naqvi

An event for medical training is being held at CMH Peshawar, and Major General Masood is distributing awards.

Climate-related challenges are growing in Pakistan, and the prime minister’s climate aide is advocating for gender-inclusive climate resilience.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News23 hours ago

Latest News23 hours agoPakistani Internet: Everything you should know about “Africa-2” contemporary cables

-

Entertainment23 hours ago

Entertainment23 hours agoHania Aamir reveals details about her troubled childhood.

-

Business23 hours ago

Business23 hours agoWith its second-largest surge ever, PSX approaches 114,000 points.

-

Latest News23 hours ago

Latest News23 hours agoWapda announces a revised timeline for the K-4 water project in Karachi.

-

Latest News23 hours ago

Latest News23 hours agoThe PPP and PML-N will confer on power-sharing arrangements in Punjab today.

-

Latest News18 hours ago

Latest News18 hours agoClimate-related challenges are growing in Pakistan, and the prime minister’s climate aide is advocating for gender-inclusive climate resilience.

-

Latest News18 hours ago

Latest News18 hours agoA Seminar on Deciphering the Influence of the Media Is Being Organized by IICR

-

Latest News18 hours ago

Latest News18 hours agoAn NIH case of wild poliovirus was discovered in Balochistan, marking the 65th confirmed case of polio.