Business

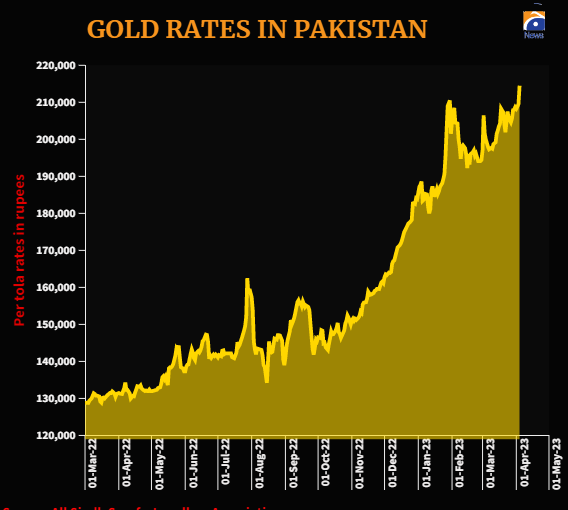

Gold jumps to all-time high of Rs214,500 per tola in Pakistan

- Gold price increases by Rs5,000 per tola.

- It has gained Rs5,200 per tola in two sessions.

- Silver price scales new peak of Rs2,450 per tola.

Gold price in Pakistan soared to an all-time high at Rs214,500 per tola (11.66 grams) on Tuesday after the rupee fell to a historic low against the US dollar in the interbank trade.

The surge was in line with the rupee movement — which plunged to an all-time low of Rs287.29 against the US dollar in the interbank market — and an uptrend in the global markets.

According to the data released by All-Pakistan Sarafa Gems and Jewellers Association (APSGJA), the price of gold (24 carats) soared by Rs5,000 per tola and Rs4,288 per 10 grams to settle at Rs214,500 and Rs183,900.

Gold is often hailed as a hedge against inflation—increasing in value as the purchasing power of the dollar declines.

Pakistan’s monthly inflation blew past forecasts in March and soared to a nearly all-time high level — 35.4% — from a year earlier, with people feeling more pain from some of the fastest rising consumer prices amid straining budgets as cost of living continues to outstrip average incomes.

Cumulatively, the precious commodity gained Rs5,200 per tola during the two sessions (Monday-Tuesday).

Investors’ attention shifted towards the precious commodity during the week as the economic tensions continue to rise amid the International Monetary Fund (IMF) reviewing external financing commitments from friendly countries before it releases bailout funds.

The delay in the revival of the programme negatively impacted the currency market which in turn is bolstering demand for gold.

Gold price moves in line with the rupee-dollar parity as the country meets almost all its gold demand through imports, and traders follow its international price in setting rates in the country.

Jewellers import the metal against the US dollar and UAE dirham before converting its price into rupees.

Moreover, a hike in seasonal demand added fuel to the rising prices in the local bullion market.

The association also mentioned that the price of gold is Rs7,000 per tola “undercost” in Pakistan, as compared to the Dubai market, showing that the Pakistani gold market was currently cheaper than the global.

Meanwhile, silver prices in the domestic market jumped to an all-time high of Rs2,450 per tola and Rs2,100.48 per 10 grams after an increase Rs100 per tola and Rs85.74 per 10 grams, respectively.

In the international market, gold price gained $12 per ounce to settle at $1,982.

Maintaining Fertiliser Price Stability: The Need for a Continuous Gas Supply to the Fertiliser Sector

Fifth Straight Cut: PM Applauds SBP’s Policy Rate Reduction

GHQ Attack Case: Prosecution Seeks Bail Cancellation of CM KP & Other Accused, Indicts 9 More

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team